The Indonesian Ministry of Energy and Mineral Resources Announces New Industry Reference Prices, New Policies Emerging One After Another

2025 February 24, the Indonesian ESDM (Ministry of Energy and Mineral Resources) issued the "Guidelines for Determining Benchmark Prices for the Sale of Metallic Minerals and Coal," with decision number 72.K/MB.01/MM.B/2025. The guidelines state two key points: “Operators holding mining business licenses and special mining business licenses in the production phase must refer to benchmark prices when selling their produced minerals or coal” and “The current benchmark prices for metallic minerals and coal are not yet fully effective and cannot serve as a reference for operators holding mining business licenses and special mining business licenses in the production phase when selling minerals or coal”. These points convey, to some extent, the intention to control nickel ore and downstream nickel product prices through the formulation and regulation of HPM prices. On

2025 March 1, ESDM issued decision number 80.K/MB.01/MEM.B/2025, titled "Reference Prices for Metallic Minerals and Coal for the First Period of March 2025," announcing the reference prices for metallic minerals (hereinafter referred to as HMA) and coal (hereinafter referred to as HBA) for the first period of March 2025. It was clarified that HMA and HBA would serve as the basis for calculating the benchmark prices for metallic minerals (hereinafter referred to as HPM) and coal (hereinafter referred to as HPB) for the first period of March 2025.

Since February, Indonesia has been introducing new policies continuously, targeting both the resource and smelting sectors, covering various aspects such as finance, foreign exchange, and industrial pricing. Just a few days ago, the Indonesian government's foreign exchange control policy attracted significant attention. On February 17, Indonesian President Prabowo issued Presidential Decree No. 8 of 2025, announcing the natural resource export foreign exchange control policy (DHE SDA), which has now been made public. So, what are the internal connections between these policies, and in what aspects might these policies continue?

Details of the above policies are as follows:

1. In the "Reference Prices for Metallic Minerals and Coal for the First Period of March 2025," the HMA prices for the first period of March 2025 were announced, including the calculation methods for 19 types of metals or ores such as nickel, cobalt, lead, zinc, gold, and chrome ore. Taking nickel metal as an example, the nickel metal price announced for this period is $15,276.33/ton, and the previous calculation method of "taking the average of the LME spot settlement prices from the 20th of the second month before the HPM period to the 19th of the previous month" was replaced with "taking the average from the 5th to the 25th of the previous month of the HPM period." According to SMM, the HMA prices will be revised twice a month in the future, instead of once at the beginning of each month. According to APNI Secretary General Meidy, the HMA price for the second period of March might be calculated as “taking the average of the LME spot settlement prices from the 26th of the previous month to the 4th of the current month of the HPM period”. This calculation formula is still under confirmation and adjustment and will be officially announced by ESDM around the 15th.

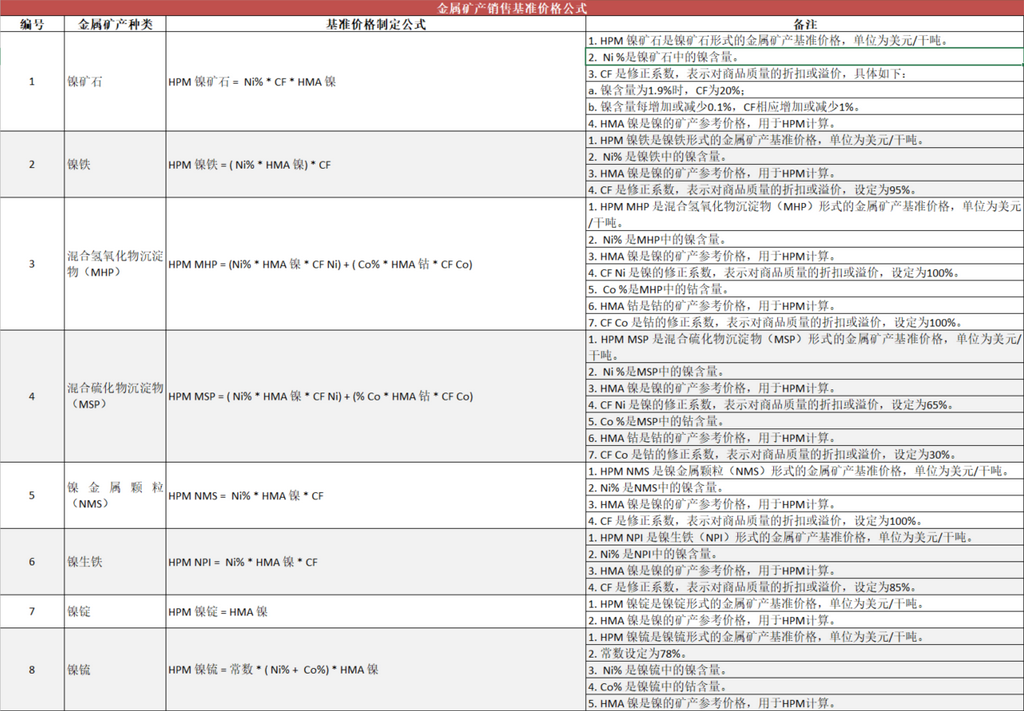

2. In the "Guidelines for Determining Benchmark Prices for the Sale of Metallic Minerals and Coal," the benchmark price formulas for 8 nickel-related products were clarified, as shown in the figure:

The calculation logic for HPM nickel ore in Indonesia remains unchanged, which is HPM nickel ore = Ni% * CF * HMA nickel. However, the HMA price has changed due to the adjustment in the calculation method. The HMA nickel price for March calculated using the previous method was $15,306.52/ton, while the HMA nickel price for the first period of March announced by ESDM was $15,276.33/ton, which is $30.19/ton lower than the previous calculation method. The overall change is relatively small. Moving forward, HPM will be revised every half month.

SMM's In-depth Analysis of the Policy Details:

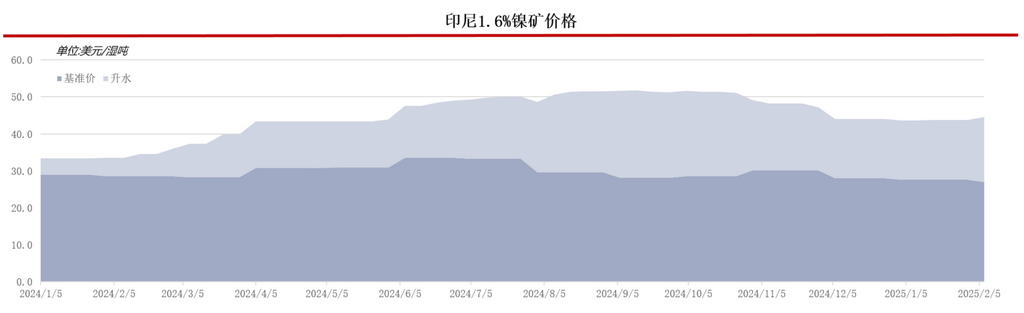

- For nickel ore: In the "Reference Prices for Metallic Minerals and Coal for the First Period of March 2025," the calculation method for HMA for metals or ores was modified, possibly due to the lag in the previous HMA calculation period, which caused the calculated HPM prices to fail to reflect the current market price trends and occasionally even move counter to the absolute prices in the nickel ore market. Taking the SMM Indonesian 1.6% grade nickel ore price as an example, as shown in the figure:

Additionally, the previous HMA revision cycle was once a month, which could not reflect mid-month price changes in the nickel ore market.

Looking ahead, HMA will be revised semi-monthly, and the calculation period will be closer to the current nickel market prices. The subsequent HPM nickel ore benchmark price may improve in terms of market feedback timeliness.

2. For other nickel products: In the "Guidelines for Determining Benchmark Prices for the Sale of Metallic Minerals and Coal," the HPM price calculation methods for 7 other nickel products besides nickel ore were newly added or clarified. However, according to SMM, the HPM prices for nickel products other than nickel ore differ significantly from actual market prices. Taking NPI as an example, HPM NPI = Ni% * HMA nickel * CF. Based on this formula, for instance, the 12% NPI price for March would be $1,558/ton, which translates to a domestic selling price of approximately 1,072 yuan/mtu. On March 4, the SMM Indonesian 10-14% high-grade NPI floor price was 984-991 yuan/mtu, with the HPM price higher than the domestic selling price. The benchmark price HPM for Indonesian nickel ore is related to the "nickel ore resource tax" “nickel ore resource tax” that domestic market participants need to pay, while most Indonesian nickel smelting products are export-oriented and are generally not subject to local VAT. Moving forward, attention should be paid to whether the government policies will apply the HPM prices to the payment of export tariffs.

3. The first three articles of the "Guidelines for Determining Benchmark Prices for the Sale of Metallic Minerals and Coal" are as follows:

Article 1: Establish benchmark prices for the sale of metallic minerals and coal, including:

a. The benchmark price formula for metallic minerals (hereinafter referred to as HPM), as shown in Appendix I, which is an integral part of this decision;

b. The reference price formula for coal (hereinafter referred to as HBA), as shown in Appendix II, which is an integral part of this decision;

c. The benchmark price formula for coal (hereinafter referred to as HPB), as shown in Appendix III, which is an integral part of this decision.

Article 2: Operators holding mining business licenses in the production phase, operators holding special mining business licenses in the production phase, and holders of special mining business licenses as extensions of contracts/agreements, including holders of contract work agreements and coal mining cooperation agreements, must refer to the HPM or HPB mentioned in Article 1 when selling their produced metallic minerals or coal.

Article 3: The HPM and HPB mentioned in Article 1 are the minimum prices for the sale of metallic minerals or coal by operators holding mining business licenses in the production phase, operators holding special mining business licenses in the production phase, and holders of special mining business licenses as extensions of contracts/agreements (including holders of contract work agreements and coal mining cooperation agreements).The regulation explicitly specifies that its targets remain the holders of "IUPK/IUP" licenses. Besides local Indonesian mining companies, most Indonesian smelters are also "IUPK/IUP" license holders. However, it remains uncertain whether the HPM price will apply to export products under this policy. Currently, the HPM prices of other products differ significantly from market pricing, and the upward price support for products like NPI is limited, which may pose challenges during the policy's implementation. How to view Indonesia's related policies going forward: The significance of implementing HPM prices. For the nickel ore sector, the current market supply and demand situation is more reflected in the PREMIUM of domestic trade ore in Indonesia. Changes in the HMA calculation method leading to HPM price adjustments may not directly impact market prices in the short term. However, if HPM prices are implemented and extended to export prices, two possibilities may arise (using high-grade NPI as an example): Possibility 1: If HPM prices are strongly enforced, requiring the market to use HPM prices as the "floor price" for settlement, it would significantly restore the sales profits of Indonesian nickel iron enterprises. According to SMM statistics, the cost of Indonesian NPI in January on Sulawesi Island was approximately $11,626/mt (Ni contained), while the average cost on other islands was $11,472/mt (Ni contained). If HPM is strongly implemented, the profit restoration may accelerate the subsequent production of nickel iron, further expanding the future supply surplus of nickel. Possibility 2: If HPM prices are extended as a reference for export prices but only serve as a basis for subsequent government tax collection, i.e., if the market transaction price is lower than or equal to the HPM price, tariffs will be paid according to the HPM standard. If the market transaction price is higher than the HPM price, tariffs will be paid based on the market transaction price. This would effectively increase the export costs for nickel iron producers. (Both scenarios are based on the assumption that HPM prices are applied to the settlement of export product sales prices.) These two policies were introduced around the same time as Indonesian President Prabowo's issuance of Presidential Regulation No. 8 of 2025, which announced the natural resource export foreign exchange control policy (DHE SDA). Although challenges may arise during implementation, it clearly reflects the Indonesian government's intention to guide nickel prices, enhance the value of Indonesian nickel products, and increase tax revenue. Since the beginning of 2025, ESDM has repeatedly stated in public interviews that it will stabilize nickel prices and ensure the value of nickel products by controlling the annual RKAB quotas. Article 7 of Presidential Regulation No. 8 of 2025 revises the requirement that 100% of natural resource export foreign exchange (DHE SDA) must be deposited in designated accounts for at least 12 months (exception: for oil and natural gas-related DHE SDA, a minimum of 30% must be deposited for at least 3 months). Whether this will be expanded to other products remains to be seen. Starting in 2025, from the launch of the SIMBARA system at the beginning of the year to the widely discussed announcement of the natural resource export foreign exchange control policy (DHE SDA), and the subsequent adjustments to HPM and HBA prices, the Indonesian government has consistently conveyed its policy intention to better control the pricing power of local resources and products, increase national tax revenue, and enhance Indonesia's economic position on the international stage. For the nickel industry, from nickel ore to smelters, the policy's regulatory intensity at each stage is becoming increasingly stringent. During this period of changes in Indonesia's foreign exchange control policies, it is crucial to pay closer attention to export-related policies to better navigate the opportunities and challenges of investing in Indonesia.